Ever wonder how much the average American actually pays for healthcare compared to someone buying insurance through the Affordable Care Act (ACA)? The numbers might surprise you.

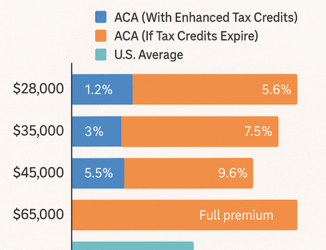

Currently, thanks to enhanced ACA tax credits, many individuals are paying a relatively manageable share of their income for coverage. Someone making around $28,000 a year pays about 1% of their income; that’s roughly $ 280 a year for a solid plan. Even at $45,000 a year, the share stays under 6%, which is actually less than what most people with employer insurance end up paying.

But here’s where things get tricky: those enhanced tax credits are set to expire. The cost for ACA enrollees could more than double overnight. That same person making $28,000 would suddenly owe about 6% of their income, or over $ 1,700 a year. For middle-income families, it could be 10% or even 20% of their take-home pay just for premiums.

Meanwhile, the average American household (with employer insurance or not) already spends about 11–12% of its income on healthcare when you count premiums, copays, and out-of-pocket costs. So, if the ACA subsidies are eliminated, many Marketplace users would actually end up paying more than the national average.

The enhanced ACA tax credits made healthcare more accessible and helped hospitals stabilize uncompensated care. Letting them expire could push millions back into the uninsured population and put even more financial strain on providers already struggling with thin margins.

At RCA, we’re here to help both hospitals and patients navigate these headwinds, connecting people to the coverage and financial assistance they need while protecting the economic stability of the health systems that serve them.

Leave A Comment

You must be logged in to post a comment.